About BPSP

Supporting bill payment aggregators to easily facilitate commercial / B2B bill payments between buyers and suppliers.

Card networks offer bill payment provider programs called Business Payment Service Provider (BPSP) or Bill Payment Provider (BPP) programs. BPSP/BPPs are often bill payment aggregators for commercial / B2B bill payments, and can help accept card payments to pay off a business invoice often when the supplier is not a card accepting merchant.

Bill Payment Service Provider

A Business Payment Service Provider (BPSP) or Bill Payment Provider (BPP) is a service provider who facilitates commercial business-to-business payments between buyers and suppliers.

Use Case

- B2B Payments : Facilitate payment acceptance for vendors and suppliers from other businesses.

Why Use BPSPs?

The BPSP program allows buyers to pay their bills with a network-approved commercial card even if the supplier is not a card accepting merchant, thereby providing more payment options for buyers. The buyer pays the BPSP with say, a Mastercard/Visa commercial card, and instructs the BPSP to pay the supplier on its behalf. The BPSP pays the supplier using a non-card method of payment.

The BPSP Model:

- Focuses on commercial or business-to-business payments, usually for invoices based on pre-negotiated terms.

- Disallows BPSPs to enable transactions for billers who do accept Visa for network-approved cards through other channels.

- Establishes contracts between BPSP and TabaPay, not the underlying sellers.

- Requires the BPSP to manage the end-to-end customer experience, processing the customer’s purchase and issuing a transaction receipt under the name of the BPSP.

- Also requires BPSPs to process customer service inquiries, refunds and disputes, though these are usually low on the basis that most payments are post-paid bills for products/services that have already been consumed or delivered.

Cost-Effective Bill Payments

If you as a business accept corporate/commercial cards, you can reduce the overall cost of payment acceptance by providing more data through TabaPay to the networks. This data, when sent to card networks such as Visa and MasterCard enables businesses to secure a much lower interchange rate.

Interested in Level 2/Level 3 processing?If you are a business with higher volumes of B2B or B2G payment volume, TabaPay can help you bring down the costs of payment processing with L2 and L3 data shared with the networks.

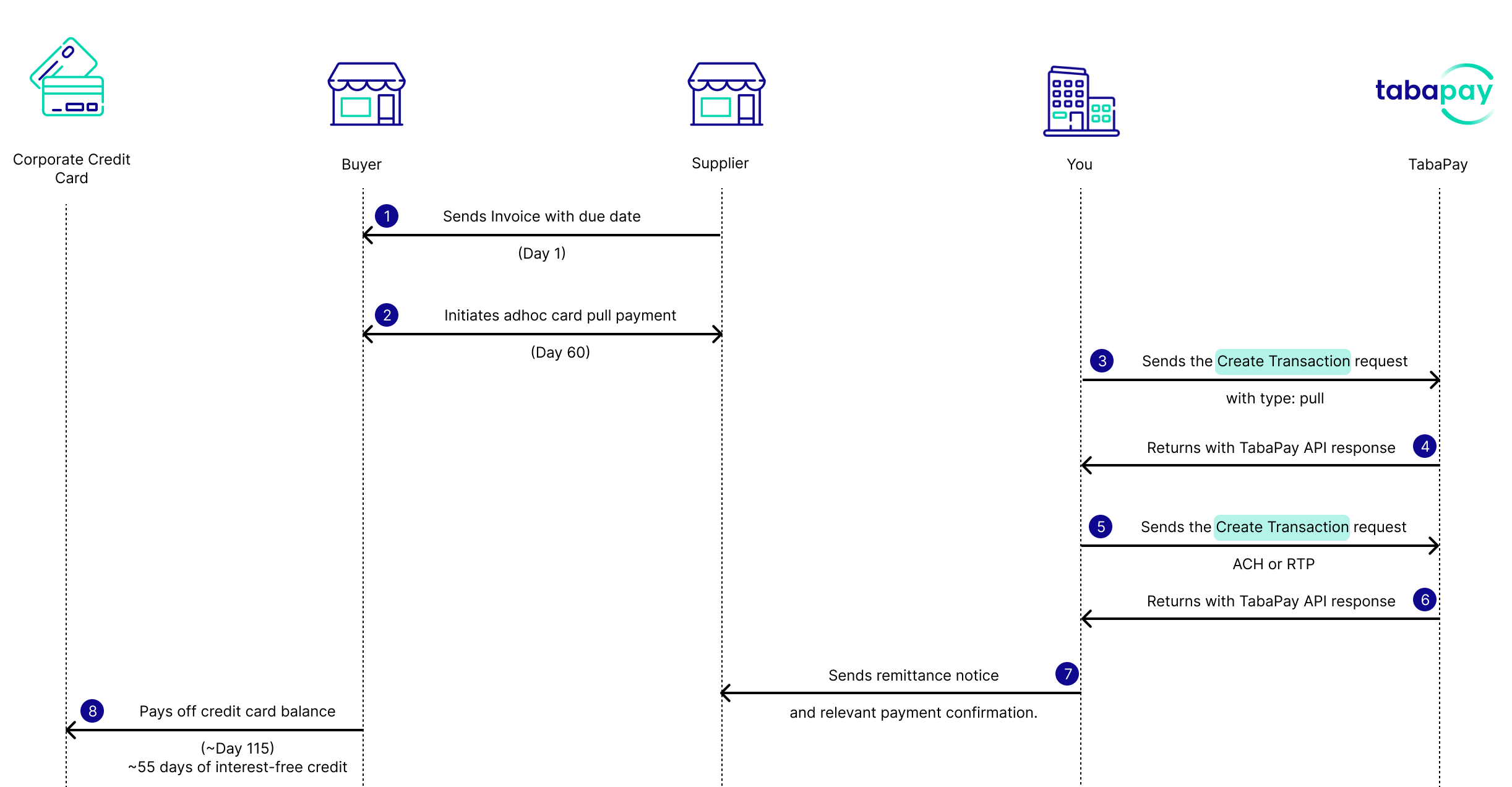

BPSP Flow

- Suppliers invoices for a payment in 60 days once they receive the purchase order from the buyer.

- Buyer (or supplier with COF) initiates the adhoc card on file pull payment before day 60.

- The BPSP integrates with the Create Transaction API request to pull funds from the Buyer's commercial card.

- TabaPay returns the API response

- You send the Create Transaction API request for an ACH, or RTP payment to the suppliers bank.

- TabaPay returns the API response.

- You send a remittance notice and the relevant payment confirmation.

- Buyer pays off their commercial credit card within the 55 day window of no interest.

How BPSP Works

See each network for requirements to include in the Create Transaction API request.

Visa

To see Visa BPSP requirements, select the Visa Requirements dropdown.

Visa Requirements

TabaPay will register you as a BPSP with Visa, and you will be required to sign a commercial agreement with Visa directly.

Overview: Effective 13 April 2024Visa will introduce new eligibility and compliance rules to the Business Payment Solution Provider payment model.

Visa Key Requirements

The following items are required for the Visa network.

Supplier Eligibility & Payment Scope

- Certify to Visa that the supplier being paid through the BPSP, conditionally accepts or does not accept Card payment for the good or service being purchased and paid by the buyer and therefore pursues payment via the BPSP.

- Permit payments to overseas suppliers. Buyers may pay suppliers in other countries via a BPSP.

- Accept payments from businesses for business expenses using Visa Commercial Cards, and through April 17, 2027, Visa Consumer Cards.

- Supplier may accept a Visa Commercial Card of their choice

- Ensure the MCC assigned to each supplier accurately describes a supplier’s business is assigned to the supplier

Consumer Card Acceptance - Until April 2027Buyers will be able to utilize their preferred Visa card (consumer or commercial) for payments as long as the applicable transaction is initiated by a business and is for a business purchase. It is important to note that consumer cards will only be accepted until April 2027.

Transaction Timing & Processing Rules

- Only perform BPSP services as a Card-Absent Environment Merchant

- Initiate transactions only after:

- The buyer confirms that goods or services have been shipped or delivered; and

- The buyer approves the payment.

- Use a secure payment process that ensures funds are deposited into individual supplier accounts.

- Process each invoice from a non-Visa-accepting supplier to a buyer is processed as a separate transaction.

Compliance, Risk & Buyer Responsibility

- Perform KYC and meet all applicable AML requirements for all suppliers, including non–Visa-accepting suppliers, before initiating transactions.

- Require a written agreement with each buyer stating that the buyer assumes all risks associated with supplier nonperformance.

Visa MCCs

- The following MCCs are eligible ONLY when the buyer utilizing the BPSP provides to Visa a valid government-issued business identification number or Taxpayer Identification Number (TIN) upon Visa request:

MCC Description 4900 Utilities – Electric, Gas, Water, and Sanitary 6300 Insurance Sales, Underwriting, and Premiums 6513 Real Estate Agents and Managers 9311 Tax Payments

Visa Restricted MCCs

Ensures that the following Merchant Category Codes (MCCs) are not eligible to be included in BPSP-supplier flows:

Note: All designated unique airline and air carrier, car rental agency, and lodging MCCs, as

specified in the Visa Merchant Data Standards Manual

| MCC | Description |

|---|---|

| 4112 | Passenger Railways |

| 4411 | Steamship and Cruise Lines |

| 4722 | Travel Agencies and Tour Operators |

| 4723 | Package Tour Operators – Germany Only |

| 4814 | Telecommunication Services, including Local and Long-Distance Calls, Credit Card Calls, Calls Through Use of Magnetic-Stripe-Reading Telephones, and Fax Services |

| 4829 | Money Transfer |

| 4899 | Cable, Satellite, and Other Pay Television/Radio/Streaming Services |

| 5962 | Direct Marketing – Travel-Related Arrangement Services |

| 5966 | Direct Marketing – Outbound Telemarketing Merchant |

| 5967 | Direct Marketing – Inbound Teleservices Merchant |

| 6010 | Financial Institutions – Manual Cash Disbursements |

| 6012 | Financial Institutions – Merchandise, Services, and Debt Repayment |

| 6051 | Non-Financial Institutions – Foreign Currency, Liquid and Cryptocurrency Assets [for example: Cryptocurrency], Money Orders [Not Money Transfer], Account Funding [not Stored Value Load], Travelers Cheques, and Debt Repayment |

| 6211 | Security Brokers/Dealers |

| 7011 | Lodging – Hotels, Motels, Resorts, Central Reservation Services [Not Elsewhere Classified][Not Elsewhere Classified] |

| 7012 | Timeshares |

| 7512 | Automobile Rental Agency |

| 8011 | Doctors and Physicians [Not Elsewhere Classified] |

| 8050 | Nursing, Home Healthcare and Personal Care Facilities |

| 8062 | Hospitals |

| 8099 | Medical Services and Health Practitioners [Not Elsewhere Classified] |

| 8211 | Elementary and Secondary Schools |

| 8220 | Colleges, Universities, Professional Schools, and Junior Colleges |

| 8241 | Correspondence Schools |

| 8244 | Business and Secretarial Schools |

| 8249 | Vocational and Trade Schools |

| 8299 | Schools and Educational Services [Not Elsewhere Classified] |

| 8351 | Child Care Services |

Reporting Obligations to Visa

- Provides annual reporting to Visa directly, including:

Reporting to VisaAll reports are due on the 10th day of the following month.

Please copy [email protected] in your emails with report submissions to Visa.

- Total Visa payment volume flowing through the BPSP

- Total Visa payment volume of overseas payments

- Breakdown of Visa payment volume by supplier MCC

- Breakdown of Visa payment volume and Transaction count by Visa product type

- Effective 13 April 2024 through 17 April 2027 Breakdown of Visa payment volume and

Transaction count of the top 100 suppliers paid via Visa Consumer Cards - Provide quarterly reporting to Visa on overseas payments including breakdown of payment volume and transaction count by country corridor (i.e. buyer country, BPSP country, and supplier country)

- Sign a separate agreement with Visa to ensure compliance with the Visa Rules, including but not limited to the above annual and quarterly reporting requirements

Mastercard

To see MC BPSP requirements, select the Mastercard Requirements dropdown.

Mastercard Requirements

NEW MasterCard Bill Payment Service Provider (BPSP) ProgramEffective 1, January, 2025, Mastercard is revising its Standards to introduce a Business Payment Service Provider (BPSP) category and related requirements for commercial business-to-business (B2B) payments between buyers and suppliers.

Under the MasterCard BPSP program, buyers may source suppliers globally, allowing buyers and suppliers to be located in different markets. Additionally, while payment from the BPSP to the supplier must be completed with a non-card method, the supplier may be a card-accepting merchant for non-BPSP transactions.

Key Requirements

The following items are required for the Mastercard network.

Registration & Commercial Model

-

BPSP is registered with Mastercard through the Sponsor Bank.

-

The BPSP must pay suppliers using a non-card payment method, even if the supplier accepts Mastercard for non-BPSP transactions.

-

The BPSP, buyer, and buyer’s commercial card issuer must be located within the acquirer’s area of use. Suppliers may be located outside that area.

Buyer Agreement & Liability Allocation

-

The BPSP must enter into a written agreement with the buyer. The agreement confirms, among other things, that chargeback rights for Goods or Services Not Provided will not apply (except when payment not properly applied to the buyer's account or a credit not processed) and requires the buyer to resolve any non-performance concerns directly with the supplier.

-

The buyer must pay the BPSP with a commercial card per the contractual agreement between the buyer and the BPSP.

Transaction Execution & Settlement Controls

-

Following the receipt of settlement funds from its acquirer, the BPSP must pay the supplier the invoiced amount as instructed by the buyer.

-

All payment origination parties: The BPSP, each buyer initiating payment through the BPSP, and the buyer's commercial card issuer must be located within the area of use of the BPSP's acquirer. Only the supplier receiving payment through the BPSP may be located outside of the BPSP acquirer's area of use.

-

The BPSP must only initiate a transaction in accordance with the buyer's payment instructions, for example, following the buyer's confirmation of the supplier's shipment of the goods or delivery of the goods or services and the buyer's approval of the payment.

-

The BPSP must submit separate transactions per invoice and use a secure process to deposit funds into individual supplier accounts. Bundling is permitted only when paying multiple invoices from one buyer to the same supplier.

Mastercard BPSP MCC

Mastercard BPSP MCCs should be categorized as the following:

| MCC | Description |

|---|---|

| 7399 | Business Services, Not Elsewhere Classified (NEC) |

American Express

To see Amex BPSP requirements, select the American Express Requirements dropdown**

American Express Requirements

American Express Bill Payment Providers (BPPs) are third parties that allow American Express Card members to make purchases at merchant establishments that may not typically accept the American Express Card.

For example, a customer can now use an American Express card to pay off medical, or dental supplies with a merchant that wouldn't typically accept Amex.

Key Requirements

The American Express Bill Payment Program (BPP) supports unique processing based on specific contracts between American Express and individual partner merchants. The merchant needs to enroll for BPP directly with American Express and they will assign a unique merchant ID.

TabaPay clients who wish to process American Express through TabaPay must provide the following information.

American Express Network MandateAmerican Express requires the following information about the merchant upon registration:

Each UBO (Ultimate Beneficiary Owners) must provide the following information:

- First Name (Required)

- Middle Name (Optional)

- Last Name (Required)

- Date of Birth (Required)

Specific merchant category codes are eligible for this program which will be addressed during the enrollment process with American Express.

American Express BPP (Bill Payment Provider)

Data Requirements for American Express BPP Programs and info required to be present for every transaction at American Express for BPP participants, refer to the following:

| Required fields |

|---|

| Bill Pay Provider name |

| Bill Pay Provider seller ID |

| Merchant / Sellers name |

| Merchant / Sellers street |

| Merchant / Sellers city |

| Merchant / Sellers state / region code |

| Merchant / Sellers country ISO code |

| Merchant / Sellers postal code |

| Merchant / Sellers phone number |

| Merchant / Sellers email address |

| Merchant / Sellers MCC |

For field descriptions, refer to Create Transaction API.

...

{

"softDescriptor": {

"address": {

"line1": "123 Street",

"city": "San Francisco",

"county": "SFC",

"state": "CA",

"zipcode": "94103",

"country": "840"

},

"phone": {

"number": "5555555555"

},

"name": "General Biller Company",

"mcc": "6012",

"email": "[email protected]"

}

}

...-

mcc: Merchant's/Seller's MCC (4-digits). Required for American Express Bill Pay Provider Program.

Note: this is not the processing MCC. This is for reporting purposes only (Amex Bill Pay Provider) -

email: Seller Email Address (max of 40 characters). Required for American Express BPP program.American Express BPSP MCCsMCC Description 0780 Horticultural and Landscaping Services 1799 Special Trade Contractors 2791 Typesetting, Plate Making, and Related Services 4011 Railroads 4215 Courier Services 5039 Construction Materials, Not Elsewhere Classified 5045 Computers, Peripherals, and Software 5046 Commercial Equipment, Not Elsewhere Classified 5047 Medical and Dental Equipment and Supplies 5051 Metal Service Centers and Offices 5065 Electrical Parts and Equipment 5085 Industrial and Commercial Machinery and Equipment 5094 Jewelry, Watches, Clocks, and Silverware 5099 Durable Goods, Not Elsewhere Classified 5111 Stationery, Office, and School Supplies 5131 Piece Goods, Notions, and Dry Goods 5137 Men's, Women's, and Children's Uniforms and Commercial Clothing 5139 Commercial Footwear 5169 Chemicals and Allied Products 5172 Petroleum and Petroleum Products 5198 Paints, Varnishes, and Supplies 5199 Nondurable Goods, Not Elsewhere Classified 7311 Advertising Services 7333 Commercial Photography, Art, and Graphics 7338 Quick Copy, Reproduction, and Blueprinting Services 7339 Stenographic and Secretarial Support Services 7349 Building Cleaning and Maintenance Services 7361 Staffing and Temporary Employment Agencies 7392 Management, Consulting, and Public Relations Services 7394 Equipment Rental and Leasing 7399 Business Services, Not Elsewhere Classified 7692 Welding Repair 7829 Motion Picture and Tape Distribution 8734 Testing Laboratories 8911 Architectural, Engineering, and Surveying Services 8931 Accounting, Auditing, and Bookkeeping Services 8999 Professional Services, Not Elsewhere Classified

Discover (Coming Soon)

Coming SoonThis product is being prepared for release. Contact TabaPay for questions.

Updated 2 months ago