Payment Account Reference (PAR)

A Payment Account Reference (PAR) is a unique identifier associated with a specific cardholder PAN and its affiliated tokens. This 29 character identification number can be used in place of sensitive consumer identification fields, and transmitted across the payments ecosystem to facilitate consumer identification.

TabaPay Clients can use PAR for transactions initiated by tokenized (accountID) and non-tokenized accounts (card info). Using the PAR value helps acquirers and merchants to manage fraud, risk, customer service, and to leverage for analytics.

You should assess how PAR affects your own Payment Card Industry Data Security Standard (PCI-DSS) compliance programs.

When cardholders conduct transactions with tokens, you may have limited or no access to the cardholder’s PAN. The establishment of a PAR associated to a PAN and all the tokens associated, helps you to uniquely identify a cardholder account without continued exposure and storage of the PAN.

Note: The PAR value is only used for uniquely referencing a PAN and is not used to replace the PAN in payment transaction processing.

Use PAR for PAN-level Rules

You can use PAR with Apple Pay or Google Pay.

Challenge: If you accept PAN and tokens (Apple Pay, Google Pay, or any network token), you will not be able to effectively set card level rules given you do not know the underlying card a token belongs to.

Note: The PAR ties a PAN to all its underlying tokens.

Solution: PAR! If you want to set PAN-based rules, or card level controls (e.g. volume/velocity rules), you can set those rules using PAR, and still be able to know that the same PAN was used even when the transaction was tokenized (Apple Pay, Google Pay, or any network token). The PAR is the same whether the payment credential was a PAN or its network token.

Note: Duplicate card check will not work. It is recommended to create client-side control that checks to see if that PAR exists across other user IDs, and if it does, then block the card from transacting.

Use Cases

- Apple Pay / Google Pay Card Updates: Use PARto connect to new tokens when cards are updated in Apple Pay are Google Pay.

- Purchase and Return with Different Card Tokens: PAR can be used to tie a purchase made with a token to a return made with a different token or with the associated card (and vice versa).

- Loyalty Points: Identify loyalty program customers and apply loyalty points to a customer’s account using PAR to connect a card across different tokens.

- Track Fraudulent Activity: Use PAR to flag and identify cards with fraudulent activity.

- Visibility with Authorization Requests: Use PAR to connect authorization requests.

- Track Card Activity Across Tokens: Providing a complete picture of cardholder activities for use by analytics.

Note: Refer to How to Use PAR for more expanded use cases.

Why Use Par?

PAR provides a consolidated view of transactions associated with a PAN and its affiliated tokens, making it easier to identify customers and their associated transactions across payment channels.

- Futureproof payments: Improve monitoring and tracking of transaction activity across the payment ecosystem.

- Improve security: Remove sensitive PAN data from multiple systems, eliminating the need to desensitize payment details.

- Drive operational efficiencies: Assign one PAR for the life of the account to connect all physical and virtual versions of a card.

- Loyalty Program Engine: Reestablish an effective payment card-linked loyalty program and improve customer recognition.

- Customer relationship manager plugin: Swiftly identify customers and their associated transactions to improve and personalize customer service.

- Risk management and fraud: Deliver metrics for fraud systems via a data element or in authorization response messaging.

How PAR Works

PAR itself is not a non-financial reference, however it is returned in the Create Transaction API response, and the Query Card API using ANI, or AVS.

Where to Find PAR

PAR will be returned in:

- Create Transaction API performed using Visa and MasterCard payment credentials, where the payment credential is either a PAN or a network token.

- Query Card API with ANI, or AVS

{

"SC": 200,

"EC": "0",

"transactionID": "TabaPay_TransactionID_",

"network": "Visa",

"networkID": "123454646545645",

"networkRC": "00",

"status": "COMPLETED",

"approvalCode": "000000",

"additional": {

"codeACI": "Y",

"codeECI": "05",

"par": "V0010056422073825495104907179"

}{

"SC": 200,

... //Refer to the complete response on the Query Card API Ref

"bin": "411111",

"last4": "1111",

"nameFI": "FORD Instiution"

},

"AVS": {

"avsID": "Q78rZrISCc3jeQORXlWtBg",

"networkRC": "85",

"networkID": "501419181602",

"authorizeID": "181602",

"codeAVS": "Y",

"codeSecurityCode": "M",

"par": "V0010013022073812195104907179",

"ANI": {

"codeMatch": "M",

"codeFullName": "M",

"codeFirstName": "M",

"codeLastName": "M"

}

}

}PAR Used with Multiple Tokens

The following table is an example of how PAR creates a link between a cardholder’s primary account number (PAN) and the various tokens created along that cardholder’s payment journey.

| Transaction Number | Description | Card Number Used | PAR |

|---|---|---|---|

| 1 | User inputs their physical card number online | Card Primary Account Number (PAN) | PARx1234 |

| 2 | User creates an account with the online retailer and stores the card number in the account on file | Token #1 | PARx1234 |

| 3 | User uses a mobile wallet (e.g., Apple Pay®, Google Pay™, Samsung Pay®) to check out | Token #2 | PARx1234 |

| 4 | User establishes recurring payments with the same online retailer (as in transaction number 2) | Token #3 | PARx1234 |

| 5 | User makes a purchase using browser autofill. | Token #4 | PARx1234 |

| 6 | User makes a purchase using Click to Pay | Token #5 | PARx1234 |

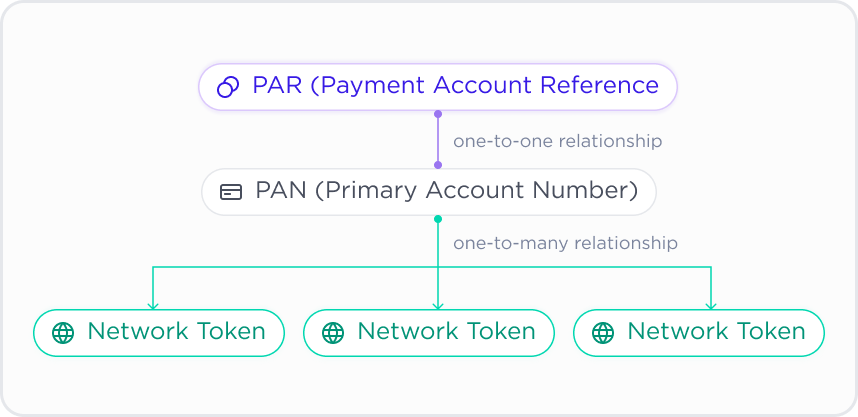

PAR is assigned to each Primary Account Number (PAN) and is used to link a payment account represented by that PAN and its affiliated payment tokens. PAR has a one-to-one relationship with an active PAN and a one-to-many relationship with the payment tokens.

PAR Used with Multiple Cards, One Account

The consistency of a Payment Account Reference (PAR) at the account level depends on how the card issuer assigns card numbers:

- Same Card Number for All Cardholders: If the issuer assigns the same card number to all cardholders on the account, the PAR will remain consistent for the entire account.

- Different Card Numbers for Each User: If the issuer assigns different card numbers to each cardholder, the PAR may vary for each user.

| Use Case | Description | PAN | PAR | Tokens |

|---|---|---|---|---|

| Issuer assigns the same card number to both cards, the same PAR represents both cards and all the associated tokens created by the primary and secondary cardholders. | Primary cardholder | x5555 | PARx1111 | Token #1 Token #2 |

| Secondary cardholder | x5555 | Token #3 Token #4 |

||

| Issuer assigns a unique card number to each card, two different PAR values are created. Each PAR value represents one set of PAN and tokens. | Primary cardholder | x5555 | PARx1111 | Token #1 Token #2 |

| Secondary cardholder | x5555 | PARx2222 | Token #3 Token #4 |

Effectiveness of PAR depends on these factors:

- The link between the PAR and the account is preserved as cards are being replaced and

- Issuers inform the token service provider (TSP) when replacing a physical card. This practice also ensures that the tokens associated with that account can continue to be used successfully.

| Use Case | Description | PAN | PAR | Tokens |

|---|---|---|---|---|

| Original card (lost and stolen) | x5555 | PARx1111 | Token #1 Token #2 |

|

| Issuer informs the network of the PAN replacement, the PAR and all existing tokens are linked to the new PAN. | Replacement card | x6666 | PARx1111 | Token #1 Token #2 |

| Issuer fails to inform the network of the PAN replacement, a new PAR is created for the replacement card and the tokens are not linked to the new PAR. | Replacement card | x6666 | PARx2222 | Tokens remain linked to PAN x5555. New tokens added to PAN x6666 will be linked to PAR x2222 |

How To Use PAR

When you receive PAR from Create Transaction API, or Query Card API, you can store PAR, and make updates whenever the network recognizes any token is associated with the PAR.

Examples of Use Cases That Leverage PAR

This section includes examples of use cases that leverage PAR.

PAR can be used to tie a transaction made with a token to a refund made with a different token or with the

associated physical card (and vice versa).

Example 1

- User makes an online transaction with Google Pay™ at TabaPay Client.

- User requests Refund from TabaPay Client on a different card.

- Since the token used to make the original purchase via Google Pay and the card used to initiate the refund have the same PAR, TabaPay can tie the transaction and refund together via PAR.

Example 2

- User makes an online transaction using the card number on file (which TabaPay Client has tokenized with TabaPay) at Tabapay Client.

- The user requests a refund with TabaPay Client using Apple Pay®.

- Since both tokens (one for the card on file and one for Apple Pay) have the same PAR, ABC Merchant can tie the purchase and return together via PAR.

Use Case #2: Loyalty Programs

TabaPay Clients can use PAR to identify loyalty program members and apply loyalty points to their users'

accounts.

Example 1

- User signs up for TabaPay Client's loyalty program. They add their card number to the account.

- TabaPay Client does a PAR lookup for the payment credential and adds it to the account.

- User makes a transaction using Apple Pay.

- Since the card number and the Apple Pay token card number have the same PAR, TabaPay Client can apply loyalty rewards to the transaction made with Apple Pay.

Example 2

- User creates an account to start earning loyalty points with a TabaPay Client who has both an online and physical presence. They add their physical card number to the account.

- The user makes a transaction using a web browser, which generated an autofill token.

- User makes a second purchase with their mobile device.

- User then goes to the TabaPay Client's physical location and makes a third purchase using Apple Pay.

- Since the PAR is the same for card numbers used with a web browser, a mobile device and Apple Pay, the TabaPay Client is able to reward the customer for all three purchases.

Example 3

- User signs up for a recurring digital service through Acme Corporation.

- User adds their card number to the account and Acme Corporation tokenizes the card number.

- User loses their physical card. Since there has been no reported fraud, the issuer issues a new physical card number and notifies the payment network on the card that the card number has been updated through the account updater process.

- TabaPay receives a new payment credential during the TabaPay Account Updater process.

- When the card gets re-used in a transaction, TabaPay returns the PAR to TabaPay Client. The PAR remains the same.

- User continues to receive loyalty points with the updated credential

Use Case #3: First Party Fraud Activity

TabaPay Clients can use PAR to identify fraudulent activity.

Example 1

- User adds their physical card number to a device wallet.

- User uses their device wallet to conduct a transaction at TabaPay Client.

- User disputes the transaction.

- TabaPay Client processes the refund to the customer.

- User removes the payment credential from their device wallet.

- User adds their card back to the device wallet.

- User uses their device wallet to conduct another transaction at TabaPay Client.

- User disputes their second device wallet transaction made at TabaPay Client

- User repeats this behavior.

- Since the PAR remains consistent across all tokens and the TabaPay Client has captured and stored PAR, TabaPay Client may identify the abusive behavior and use that information in the dispute process.

Source: US Payments Forum White Paper, 2024

FAQs

No, PAR is a value used only to reference a PAN and is not used to replace the PAN in payment transaction processing.

2. Is PAR consistent for the same card, or across re-issuance?

Yes to both. PAR identifies the underlying card account, so it stays the same across transactions for that card, including when a token is reissued, since PAR is tied to the account rather than the token.

3. Is PAR returned on every transaction for every network?

No, not for every network. PAR is returned on Visa and Mastercard transactions, but usually not when a debit transaction is routed over an alternate PIN-debit network.

Updated 23 days ago