Account Name Inquiry (ANI)

Verify the account holder.

Account Name Inquiry (ANI) helps fight against the growth in account takeover fraud and authorized push payment scams, market demand, and increasing concern from governments and regulators by verifying the official name of the account holder. In an ANI check, the customer provided name is checked against the name that the issuer has on file for the card.

Request to enable at TabaPay Support or [email protected].

Use Cases

You can consider using ANI as part of a multi-layered approach for better account verification, fraud and scam reduction, and to enhance other know-your-customer (KYC) processes.

- Adding Payment Methods to Digital Wallets: Confirm user information for adding a new payment method to digital wallets for an extra layer of verification to prevent unauthorized pull payments.

- Loan funding: check the name of a card before pushing funds to a card on your customers account.

- Adding Cards to Push to Card Workflow: Validate users’ names when adding a card to any user account holding funds to prevent unauthorized push payments.

- Online Marketplace: Validate user identity pre-transaction, to help ensure secure transactions and reducing fraudulent activities on the platform.

- Account Reactivation: Use ANI in a reactivation process for any dormant accounts that may be at risk for for fraud.

Why Choose ANI?

- Verify the cardholder’s name helps reduce fraud, especially in push and pull transactions like AFT and OCT.

- ANI benefits cardholders, merchants, wallet providers, payout operators, and any payment flow participant wanting a layer or verification.

- ANI works independently of the financial transaction, and can work with with Address Verification Service (AVS) or CVV2 as a means to triangulate the customer as an entity that is the true owner, or authorized user of the card.

Available Markets

Visa, and Mastercard ANI are available in both US and Canada. Discover coverage may be limited due no current Discover issuer mandates. For Issuer Support, refer to ANI Availability FAQs.

ANI Workflow

Using ANI, a customer-entered name is checked against the name held by the issuing bank. This check can occur:

- During customer onboarding: Verify account names to insure bolster KYC processes.

- Just before a transaction: Verify names right before specific high ticket transactions.

- Periodically: Ongoing KYC maintenance.

- On an ad-hoc basis: Verify names when account information or payment methods are updated.

ANI Example Flow

No ANI Discover Network Issuer MandateANI return rates depend on issuer participation. Because Discover does not currently require issuer participation, ANI coverage may be more limited on Discover transactions than on Visa or Mastercard.

ANI Match Key

| Match Type | Description |

|---|---|

| Match | Very close or exact match (e.g., minor spelling mistake) |

| Partial Match | Potential risk, seek additional checks/retry |

| No Match | High risk, seek additional checks/retry or block card |

| Not Supported | Issuer does not support ANI |

-

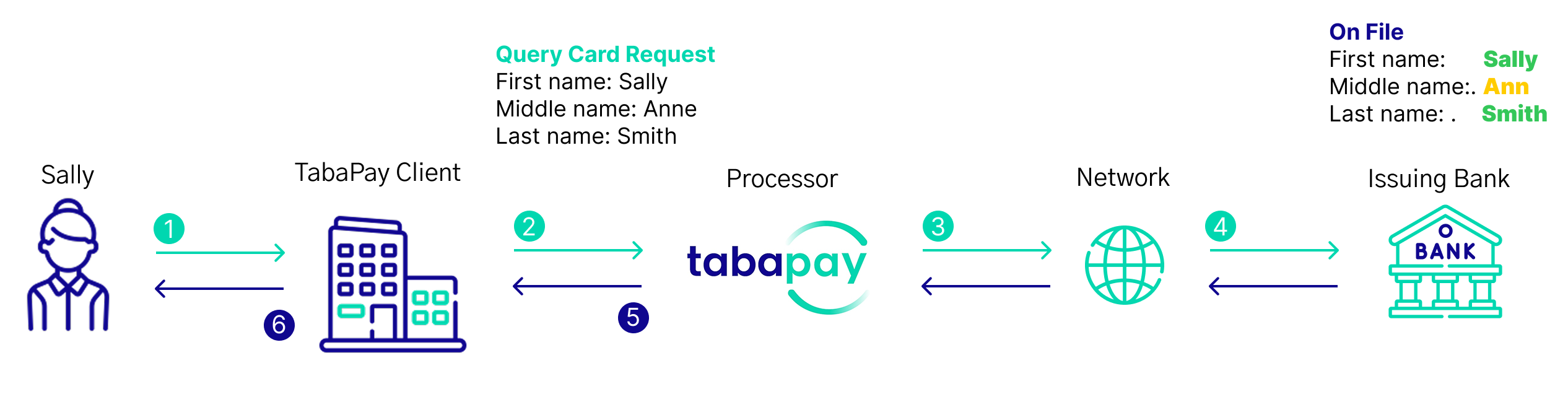

Name Collection: TabaPay Clients collect name from their customer.

-

Query Card API Request: You send the Query Card API request as part of your customer onboarding or periodic account check process. This generates a zero-dollar authorization with the cardholder’s first, middle, and last name, and other credentials for checking such as CVV2 and cardholder billing Address. TabaPay will add the card details and send to the card network.

-

Card Network Validation: TabaPay reaches out to the Card Networks to perform ANI.

-

Issuer Confirmation: The network in turn reaches out to the issuing bank to fetch the corresponding cardholder name for the payment card/token. The card network then performs a match and obtains match results.

-

Query Card API Response: You receive the API response from TabaPay with the name match results. The name match result is broken down into an overall match result.

Visa Match Results

Visa results include individual name match result for each of the

first,middleandlastnames provided. Each match result is either a Match, Partial Match or No Match For more info on responses, refer to Visa and Discover Match Name Fields.

Mastercard Match Results

Mastercard results include a full name match result with

codeFullName. The full name match result does have a Match, Partial Match or No Match. For more info on responses, refer to Mastercard Match Name Fields.

Discover Match Results*

No ANI Discover Network Issuer Mandate

ANI return rates depend on issuer participation. Because Discover does not currently require issuer participation, ANI coverage may be more limited on Discover transactions than on Visa or Mastercard.

Discover results (similar to Visa) include individual name match result for each of the

first,middleandlastnames provided. Each match result is either a Match, Partial Match or No Match For more info on responses, refer to Visa and Discover Match Name Fields.*Note: Discover may have more limited ANI coverage than than on Visa or Mastercard due to a lack of Discover mandates for participating issuers.

-

TabaPay Client Decisioning: On receipt of the name match result, the system that triggered the request, along with the account verification, interprets the match result may follow a particular fraud prevention routine defined by the TabaPay Client.

For example, the system may: log a name match success, alert their internal systems to a name match fail, layer the match result with other fraud detection tools and act accordingly, flag the fail to a manual queue or operator, request a (limited count) retry, prevent the transaction from happening, etc. It is up to the TabaPay Client to configure this logic.

ANI Decisioning

The following decisioning matrix is a recommendation, however you may develop your decisioning logic based on the best fit for your business and use case. For full descriptions of match results, refer to ANI Response Codes.

| Match Result | Example Decisioning |

|---|---|

| Matched | If a name verification has produced a Note: ANI is one of the many layers of security that TabaPay Clients have, and it is up to the clients' discretion to use these available tools. |

| Partial Match | If a Partial Match is obtained, TabaPay Clients should leverage their own risk-based approach / risk criteria before proceeding, or request additional information or retries from their customer before proceeding with subsequent transactions |

| No Match | The TabaPay Client may choose not to proceed with subsequent transactions |

How ANI Works

Get started with ANI by integrating with the TabaPay API.

Prerequisites

To request to enable ANI, contact TabaPay Support, or email [email protected].

General API Prerequisites

If you are using TabaPay Tokens for Source Account information, be sure to grab the accountID originally generated from Create Account.

Clients handling sensitive card data must comply with Payment Card Industry Data Security Standards (PCI-DSS).

Note: All requests should be in a compressed format.

1. Query Card API

TabaPay Query Card API returns the match results on Name as received from the card networks.

Visa ANI Key Fields

- codeMatch - for the overall match result

- codeFullName - for the match result on the Full Name provided

- codeFirstName - for the match result on just the First Name

- codeMiddleName - for the match result on just the Middle Name

- codeLastName - for the match result on just the Last Name

MC ANI Key Fields

- codeMatch - for the overall match result

- codeFullName - for the match result on the Full Name provided

Discover ANI Key Fields

See Discover ANI Key Fields

Discover may have limited network coverage due to a lack of mandates for participating Discover issuers.

- codeMatch - for the overall match result

- codeFullName - for the match result on the Full Name provided

- codeFirstName - for the match result on just the First Name

- codeMiddleName - for the match result on just the Middle Name

- codeLastName - for the match result on just the Last Name

Request

See how the request includes the query parameter ?ANI. This example also includes AVS.

https: //FQDN/v1/clients/ClientID/cards?ANI+AVSResponse

The Visa, MC, and Discover* ANI Query Card response is shown in the AVS.ANI object.

*Note: Discover may have limited support due to no Discover issuer mandates.

{

"SC": 200,

"EC": "0",

"card": {

"pull": {

"enabled": true,

"network": "Visa",

"type": "Credit",

"regulated": true,

"currency": "840",

"country": "840"

},

"push": {

"enabled": true,

"network": "Visa",

"type": "Credit",

"availability": "Immediate",

"regulated": true,

"currency": "840",

"country": "840"

},

"bin": "411111",

"last4": "1111",

"nameFI": "FORD Instiution"

},

"AVS": {

"avsID": "ShwI3tMDgIkfWJFkFx48lg",

"networkRC": "85",

"networkID": "422515122202",

"authorizeID": "122202",

"codeAVS": "Y",

"codeSecurityCode": "M",

"par": "V0010013022073812195104907179",

"ANI": { <-------- ANI Here

"codeMatch": "M",

"codeFullName": "M",

"codeFirstName": "M",

"codeLastName": "M"

}

}

}{

"SC": 200,

"EC": "0",

"card": {

"pull": {

"enabled": true,

"network": "MasterCard",

"type": "Debit",

"regulated": false,

"currency": "840",

"country": "840"

},

"push": {

"enabled": true,

"network": "MasterCard",

"type": "Debit",

"availability": "Immediate",

"regulated": false,

"currency": "840",

"country": "840"

},

"bin": "222300",

"last4": "0011",

"nameFI": "Obvious Financial Institution"

},

"AVS": {

"avsID": "jCofbJ4TCUXMwECNLgmjtw",

"networkRC": "05",

"networkID": "1171432030918",

"codeAVS": "N",

"codeSecurityCode": "N",

"par": "5001AJ7BWBMW0ML5RUYTQ8KDVRH2D",

"ANI": {

"codeMatch": "M",

"codeFullName": "M"

}

}

}//Discover may have limited support due to no Discover issuer mandates.

{

"SC": 200,

"EC": "0",

"card": {

"pull": {

"enabled": true,

"network": "Discover",

"type": "Debit",

"regulated": true,

"currency": "840",

"country": "840"

},

"push": {

"enabled": false

},

"bin": "601111",

"last4": "1117",

"nameFI": "Bank No"

},

"AVS": {

"avsID": "hVkcZS0TCU9CL3yUh0nHmQ",

"networkRC": "85",

"networkID": "2026050718424678000",

"authorizeID": "184246",

"resultText": "NOT DECLINED",

"codeAVS": "Y",

"codeSecurityCode": "M",

"par": "V41111111114589CED5703F989F79",

"ANI": { <-------- ANI Here

"codeMatch": "M",

"codeFullName": "M",

"codeFirstName": "M",

"codeLastName": "M"

}

}

}The example includes the ANI object the contains codeMatch, codeFullName, codeFirstName, and codeLastName.

Using ANI with AVSClients are encouraged to grab the avsID from the Query Card API response, and use it in the Create Transaction API request. This would not verify users again during the transaction, but would help track and monitor efficacy of both AVS and ANI on processing.

2. ANI Results

Please refer ANI Response Codes for the match results you will obtain as a result of the verification.

ANI Compliance

- The name used in the ANI service is the name of the cardholder that the card issuer has on file and that is linked to the associated card. This is usually, but not always, the name on card. It is also usually referred to as the legal name.

- Prior to performing an ANI name verification, the merchant, originator or cardholder should be made aware in card onboarding or registration, that they must provide the name that their issuing bank holds for them. If a cardholder changes their name, marries, uses nick-names or abbreviations, without informing their issuing bank, ANI is likely to return a partial or no match result. Some, but not all, issuers hold multiple names on a card account PAN, such as both married and maiden name.

- Visa and Discover support a first, middle and last name match, and Mastercard provides fullname match. For both, at a minimum, the last name must be provided.

- All three names should be used wherever possible. You can only supply one name set at a time (First/Middle/Last name) for matching, per Query Card API request.

- If the issuer holds more than one name set on a single card account, or PAN, then the issuer will perform checks against each name on file, and return the most viable, or positive match result.

Recipes

Updated 3 months ago