Partial Authorization Service

Authorize what you can and reduce Non-Sufficient Funds (Card Network Response Code 51) declines

TabaPay’s Partial Authorization (Auth) Service enables you to accept available remaining funds on a card, even when the full transactions cannot be approved. You can use Partial Auth instead of declining a transaction when the card’s available balance is not sufficient, and the issuer approves a portion of the original amount requested.

You can then adjust your payment flow for to collect the remainder of the transaction amount to be paid by additional customer payment methods (e.g. split-tender).

Request to enable at TabaPay Support or [email protected].

Use Cases

While prepaid and debit cards are used for instant pull payments, what happens if they do not have enough funds to cover the full transaction amount?

- Prepaid / Debit Visa/MC Cards: Process the available balance and then charge the remaining transaction amount to a secondary card during an online payment. Reduce cart abandonment, failed bill payments, and lost revenue—especially for use cases with prepaid or low-balance debit cards.

- Utility Payments: Avoid declined utility payments by accepting partial payments to cut down utility bills or vendor invoices when the customer attempts to pay the full amount.

- Account Funding Transaction (AFT): Funds are debited from an account holder to load onto another financial account.

Enable Partial Auth

TabaPay Partial Authorization Service is an opt-in service for TabaPay Clients. It must be configured in two ways:

- Set-up forMID-Level: Contact TabaPay to enable at the Merchant ID (MID) level

- API Request Parameter: In each Create Transaction API request set

partial: trueto enable partial authorization.

Supported Card BrandsVisa and MasterCard are both supported for Partial Auth. However, partial approvals will be dependent on the card issuer.

Partial Authorization Payment Flow

Customer Example

A customer wants to load $100 dollars into their favorite app, but only has $75 in the available balance.

✅ With Partial Authorization: With partial authorization, the customer's transaction is approved by the issuer for only the available balance of $75.

❌ Without Partial Authorization: The customer's authorization is declined by the issuer due to insufficient funds.

Recommended Flow

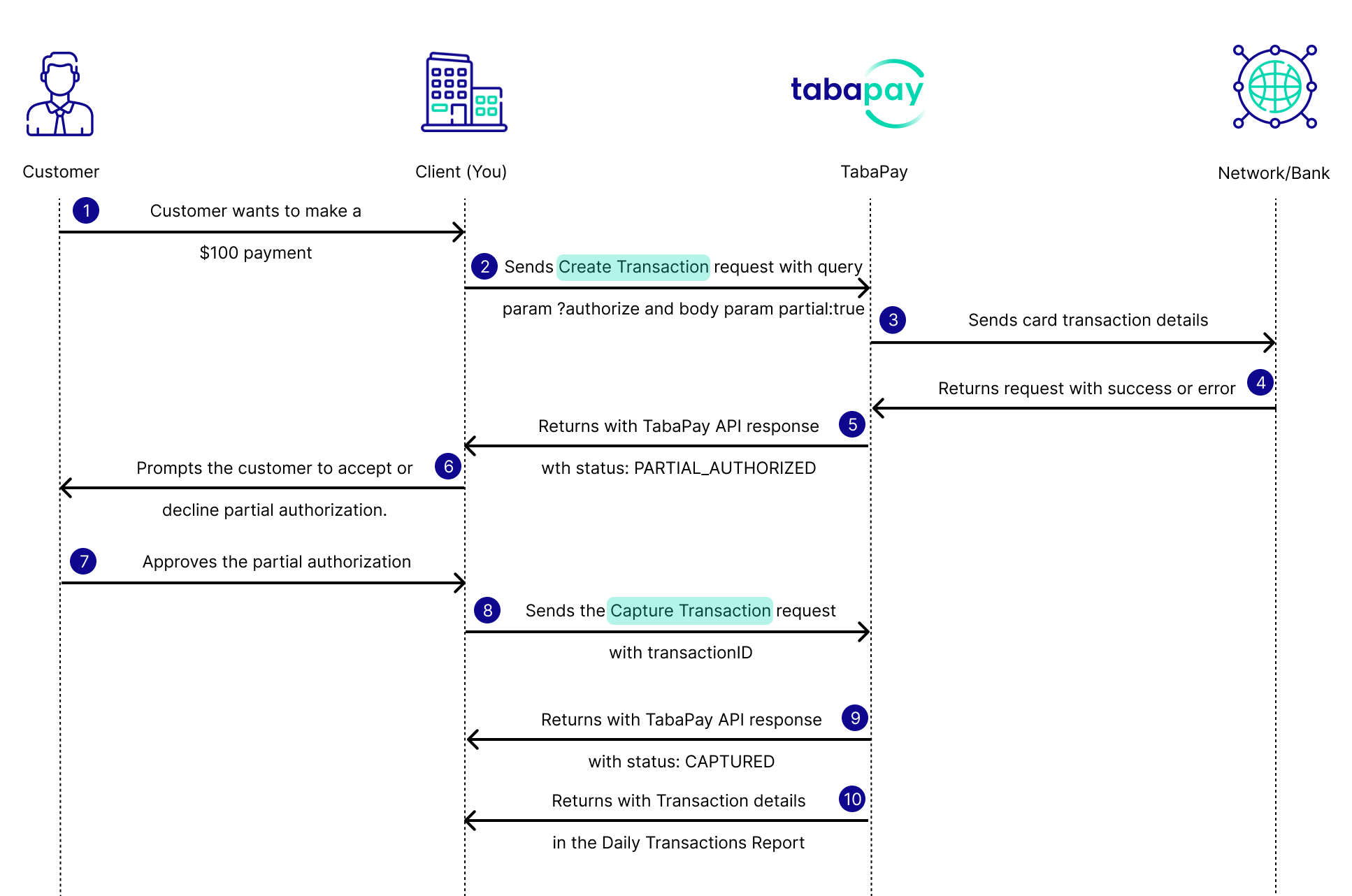

The recommended flow includes Authorize & Capture to prompt the customer to accept the partial authorization mid-flow. If declined, the transaction can be voided.

- The customer presents a card to be used for the pull transaction. Initiates a transaction of $100.

- You send out the Create Transaction API Request which includes the Partial Authorization indicator and query param

?authorize. - TabaPay sends the transaction to card network with the partial authentication indicator turned ON for the transaction.

- Network returns with a success or error.

- TabaPay returns with status:

PARTIAL_AUTHORIZED. - You prompt the customer to accept or decline the partial authorized amount.

- Customer approves the partial authorized.

- You send the Capture Transaction API request with the transactionID.

- TabaPay returns with API response with status:

CAPTURED, and remaining amount of $75. - TabaPay later sends the transaction details in the Daily Transactions Report.

Note: This process ensures your customer is satisfied with the partial authorization. If the customer does not wish to complete the sale, you can initiate a void with Delete Transaction API

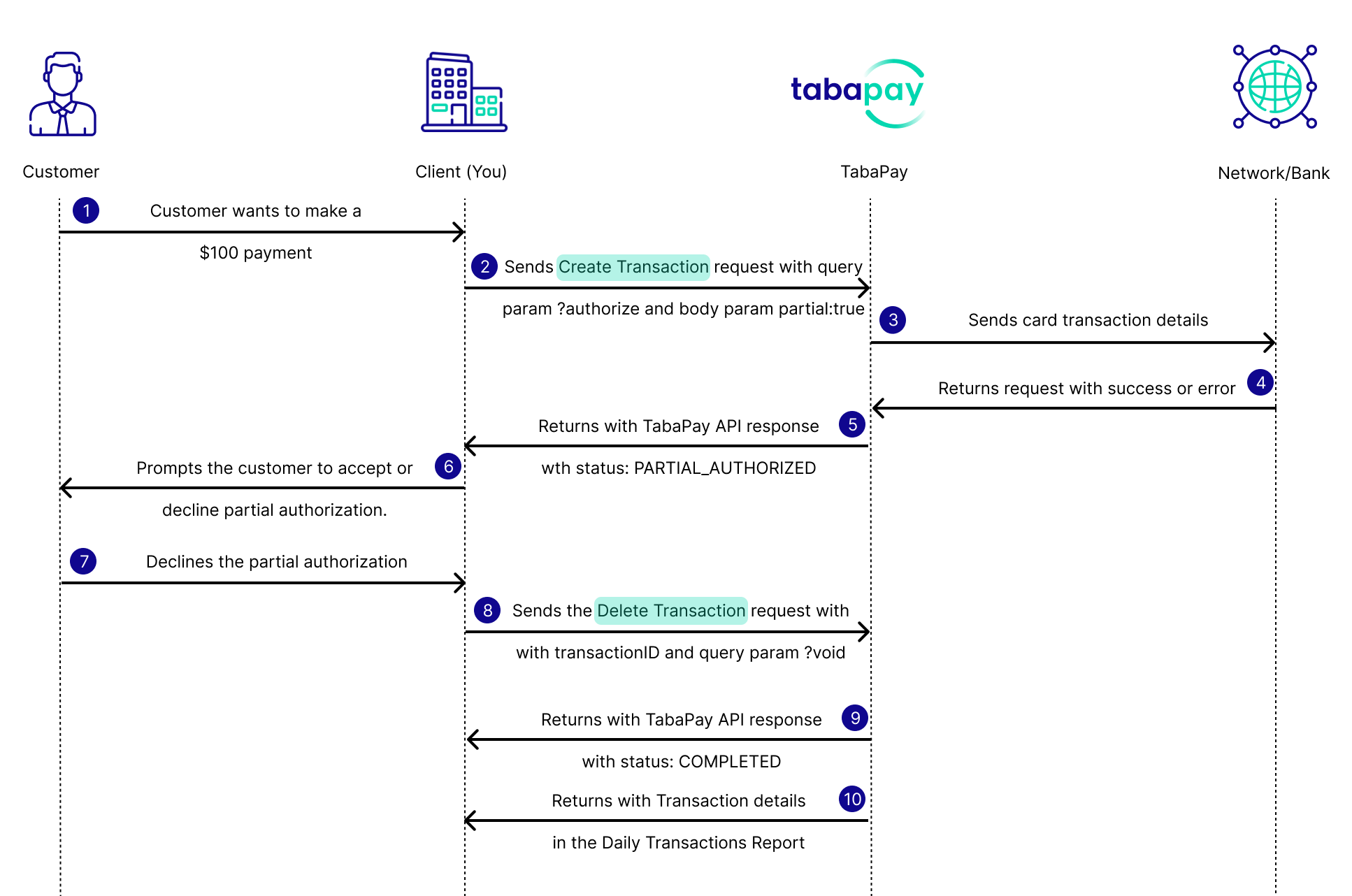

Recommended Flow - Failure Path

In the case where a customer may refuse to accept a partial authorization payment, you will void the payment with Delete Transaction API and query parameter ?void

- The customer presents a card to be used for the pull transaction. Initiates a transaction of $100.

- You send out the Create Transaction API Request which includes the Partial Authorization indicator and query param

?authorize. - TabaPay sends the transaction to card network with the partial authentication indicator turned ON for the transaction.

- Network returns with a success or error.

- TabaPay returns with status:

PARTIAL_AUTHORIZED. - You prompt the customer to accept or decline the partial authorized amount.

- Customer declines the partial authorized.

- You send the Delete Transaction API request with the ?void query parameter.

- TabaPay returns with API response with status:

CAPTURED. - TabaPay later sends the transaction details in the Daily Transactions Report.

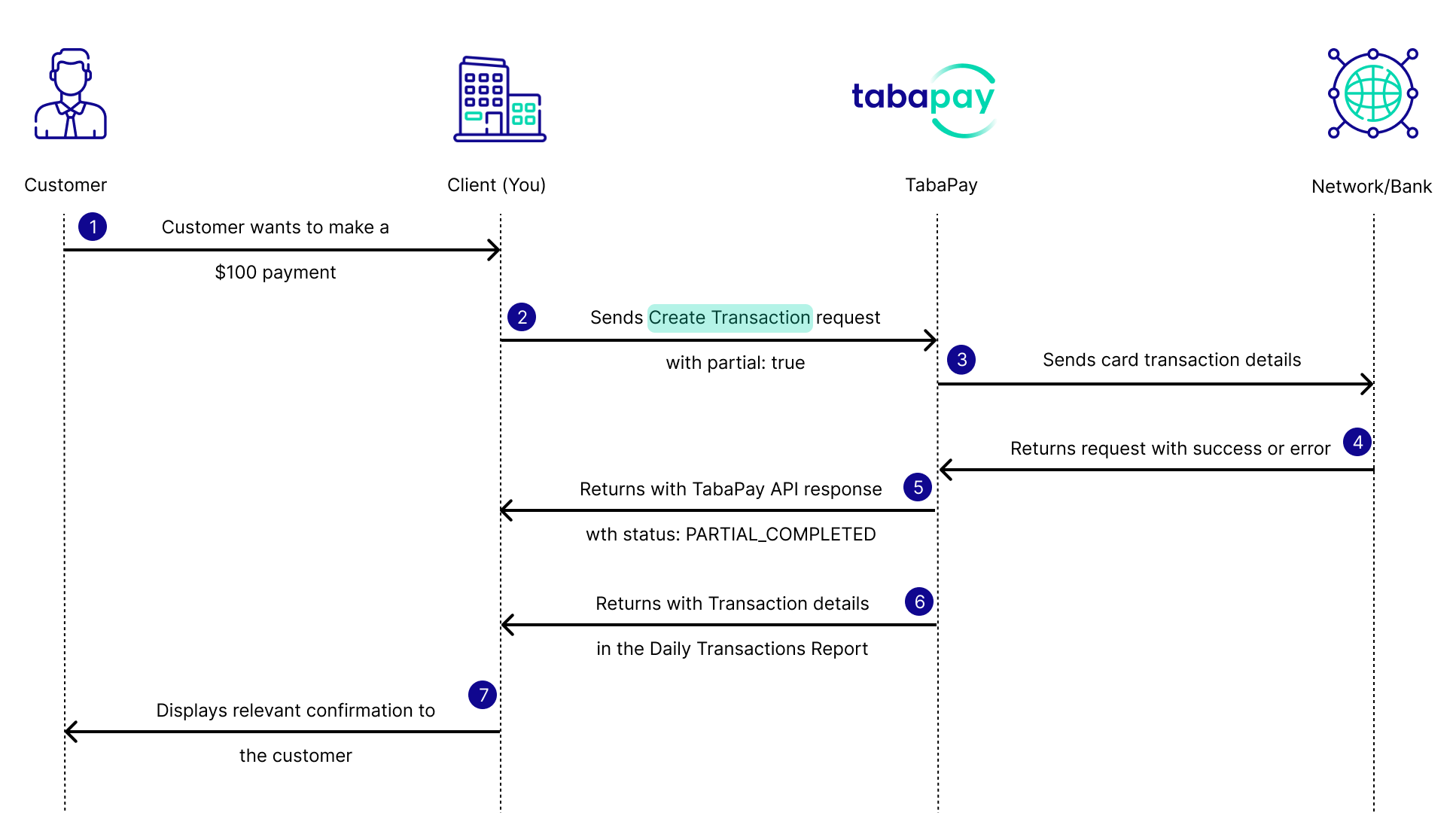

Alternative Flow

For the alternative flow, customers' should be prompted before making the payment to accept any partial authorization that will be automatically charged.

- The customer presents a card to be used for the "pull" transaction. Initiates a transaction of $100.

- You send out the Create Transaction API Request which includes the Partial Authorization indicator.

- TabaPay sends the transaction to card network with the partial authentication indicator turned ON for the transaction.

- Network returns with a success or error.

- TabaPay returns with status:

PARTIAL_COMPLETEDand remaining amount of $75.00 - TabaPay later sends the transaction details in the Daily Transactions Report.

How Partial Auth Works

The request and response field descriptions can be found at Create Transaction API.

Example Amounts vs Sandbox

The example amount values shown here may be higher than client default limits in sandbox. To increase limits, refer to Adjusting Limits.

Recommended Flow

1. Create Transaction Request

To initiate the recommended flow for partial auth indicate partial: true in the pullOptions object and include ?authorize as a query parameter in the URL.

https://{{FQDN}}/v1/clients/{{ClientID}}_{{SubClientID}}/transactions/:transactionID?authorize

Note: This displayed example includes a SubClientID.

{

"accounts": {

"sourceAccount": {

"card": {

"accountNumber": "4111111111111111",

"expirationDate": "202712",

"securityCode": "245"

},

"owner": {

"name": {

"first": "Payer",

"last": "Name"

}

}

},

"destinationAccountID": "5N0zwyQ8jnbiAWRjzwczlR"

},

"pullOptions": {

"partial": true

},

"referenceID": "1kdev0924",

"type": "pull",

"amount": "100.00"

}2. Create Transaction Response

To identify a partial authorization response, notice the partialAmount field, and the status field with PARTIAL_COMPLETED.

{

"SC": 200,

"EC": "0",

"transactionID": "5N0zwyQ8jnbiAWRjzwczlR",

"network": "Visa",

"networkRC": "00",

"networkID": "2026022721221555232",

"status": "PARTIAL_AUTHORIZED",

"approvalCode": "212215",

"AVS": {

"codeSecurityCode": "M"

},

"additional": {

"par": "V41111111114589CED5703F989F79"

},

"card": {

"last4": "5556",

"expirationDate": "202708",

"nameFI": "FORD Instiution"

}

}In the case where a customer declines to accept a partial auth for the remaining balanace, you can void a transaction using the query parameter ?void with the transactionID.

https://{FQDN}:{PORT}/v1/clients/{ClientID}_{{SubClientID}}/transactions/{TransactionID}?void3. Capture Transaction Request

Following the authorization, if the customer has approved of the partial amount charge, use Capture Transaction API and include the transactionID as a path parameter.

https://{{FQDN}}/v1/clients/{{ClientID}}_{{SubClientID}}/transactions/:transactionID

4. Capture Transaction Response

{

"SC": 200,

"EC": "0",

"referenceID": "1kdev022726",

"network": "Visa",

"networkRC": "00",

"networkID": "2026022721221555232",

"status": "AUTHORIZED",

"approvalCode": "212215",

"amount": "0.09",

"last4": "5556"

}Alternative Flow

1. Create Transaction Request

To indicate a partial authorization transaction, partial: true is required within the pullOptions object.

"accounts": {

"sourceAccount": {

"card": {

"accountNumber": "4111111111111111",

"expirationDate": "202712",

"securityCode": "245"

},

"owner": {

"name": {

"first": "Payer",

"last": "Name"

}

}

},

"destinationAccountID": "X4hdh63MBrUFyDIWVaUOdO"

},

"pullOptions": {

"partial": true

},

"referenceID": "1kdev0924",

"type": "pull",

"amount": "100.00"

}2. Create Transaction Response

To identify a partial authorization response, notice the partialAmount field, and the status field with PARTIAL_COMPLETED.

{

"SC": 200,

"EC": "0",

"transactionID": "X4hdh63MBrUFyDIWVaUOdO",

"network": "Visa",

"networkRC": "00",

"networkID": "402104171109",

"status": "PARTIAL_COMPLETED",

"approvalCode": "210558",

"partialAmount": "75.00",

"card": {

"last4": "1111",

"expirationDate": "202712",

"nameFI": "Whoop I.E. Institution"

}Partial Auth Compliance

- Only charge what was approved. You must process exactly the amount the issuer approved — no more.

- If the customer agrees, collect the remaining balance with another payment method (split-tender).

- If the customer cancels, send an authorization reversal to release the approved funds.

- Communicate clearly on the UI what was approved and what remains unpaid.

FAQs

1. How do we determine when the remaining amount from a partial authorization is not approved by the cardholder?

Based on Network Compliance Requirements, a disclosure should be displayed and it must obtain the Cardholder’s express informed consent to an agreement.

For more information, refer to the Disclosure and Agreement Section for Partial Payments.

You can also use Authorize & Capture along with Partial Auth on any dual message network to void transactions with status PARTIAL_AUTHORIZED before the recommended timeframe.

2. Are all card brands supported for partial authorization service?

Visa and MasterCard prepaid and debit cards are supported for partial authorization service. However, approvals will depend on the Issuer.

3. Do all issuers support partial authorization?

All Visa prepaid issuers and all acquirers are required to support partial authorization, and an increasing number of debit issuers support the service as well.

4. A customer performs Visa transaction for $100, but only has a balance of $80 available. What happens when partial authorization is supported?

- Create TransactionAPI Request: Includes transaction amount of $100 and the partial authorization indicator is ON.

- Create TransactionAPI Response: Includes a status of

PARTIAL_COMPLETED, orPARTIAL_AUTHORIZED(Auth & Cap + Partial Auth). - Retrieve TransactionAPI Request: Includes the transactionID from the Create Transaction Response.

- Retrieve TransactionAPI Response: The partially authorized amount of $80, and the original transaction amount of $100 is returned back in the retrieve transaction response.

5. When do TabaPay Clients reverse Partially Approved transactions?

Here are a few examples:

- When the customer does not offer additional funds to complete the transaction amount and the sale is canceled.

- The customer abandons a sale.

- The transaction is subsequently voided or cancelled for various reasons.

6. Can partial authorizations be used for both face-to-face and e-commerce transactions?

Yes. Partial authorization transactions can be used in both face-to-face and e-commerce environments. Additionally, all merchants, including mail order/telephone order and e-commerce merchants, must support sending a reversal of the partial authorization if the cardholder does not complete the purchase with another form of payment or transaction is subsequently voided or cancelled depending on their use case and context.

7. Why can't I transact amounts of $100 or $75 in Sandbox?

Client Sandbox limits may be lower by default to only transact $0.25 or lower to test. To increase limits, refer to Adjusting Limits.

Recipes

Example Report

Updated 3 months ago