Overview of RTP by TCH

A way to send funds to other US bank accounts instantly.

Real-Time payments (RTP ) network from The Clearing House (TCH) is an instant payments platform that allows financial institutions to clear and settle payments between them in real-time.

*Receive only model or enable alongside Send

TabaPay is a registered Technology Provider of Real-Time Payments over the RTP network. Through RTP, you can conveniently send and request payments directly from bank accounts at participating FDIC institutions 24/7, and to receive and access funds sent to them over the RTP network immediately.

Request to enable at TabaPay Support or [email protected].

Use Cases

- Business to Business (B2B) Payments: Send a Real-Time Payment (RTP) to suppliers and contractors, improving cash flow management and operational efficiency.

- Consumer Payments to Businesses (C2B): Customers can pay for goods and services in real-time, beneficial for last-minute or time-sensitive payments like utility bills or tax payments to avoid late fees.

- Person-to-Person (P2P) Transfers: Individuals can transfer money instantly to family or friends, whether for splitting bills, gifting, or urgent financial support.

- Account-to-Account (A2A) Transfers: Allows users to move funds between their accounts at different financial institutions instantly, which is particularly useful for managing liquidity and investment opportunities.

- Government to Citizen (G2C) Payments: Governments can disburse payments such as tax refunds, social security benefits, and emergency aid directly to citizens' bank accounts with immediacy.

Why Use RTP?

- 24/7 Access: RTP network operates round the clock.

- Immediate Availability of Funds: Recipients receive payment within seconds of the sending bank initiating the transaction (except where necessary for risk management or legal compliance purposes).

- Irrevocability: Once the payment has been authorized and submitted to the RTP network it cannot be recalled by the sender.

- Coverage: The RTP network is a growing network of FDIC institutions providing an enviable coverage of sending and receiving banks.

- More Data: RTP network provides messaging that enables a request for payment of a bill or invoice.

- Convenience: Customers of RTP network financial institution participants are able to initiate payments from their existing accounts.

- Cash Flow Control – Instant payments gives customers more control over cash flow

The RTP Ecosystem

Sender: The person or company that wishes to send a payment

- Initiates the request and receives a response through a channel such as mobile/web

Sender Bank: The Bank whose customer wishes to send a payment

- Manages the DDA of the sender

- Maintains sufficientfunding with the RTP Network

TPSP (TabaPay Service Provider) The third- party institution connecting the Financial Institutions (FIs) and/ its core or ledger system with RTP Network

- Manages the DDA of the sender

- Maintains sufficientfunding with the RTP Network

The Clearing House (TCH): RTP network for routing and settling payments between FIs

- Creates and processes the payment messages

- Forwards the payment to the RTP Network

TPSP: The third- party institution connecting the FIs and/ its core or ledger system with RTP Network

- Creates and processes the payment messages

- Posts the payment for the receiver

Receiver Bank: The Bank that receives the payment for its customer's account

- Manages the DDA of the receiver

- Sends a receipt response

Receiver: The person or company that receives the payment

- Receives the payment and able to see the details through a channel such as mobile/web app

Differences between RTP and ACH

For cost related inquiries, Contact Support or email [email protected]. For more info on RTP vs ACH, refer to ACH/RTP.

| RTP | Same-Day ACH | ACH | |

|---|---|---|---|

| Settlement Time | Immediate | Same business day | 2-3 days |

| Supported directions | Credit Push Only (Can be requested too) |

Credit and Debit | Credit and Debit |

| Bank Coverage | All banks in the RTP network | All | All |

| Transaction Limit | $10 million | $1 million (effective March 18, 2022) |

RTP Sponsor Bank - Simplified

| Account | Definition |

|---|---|

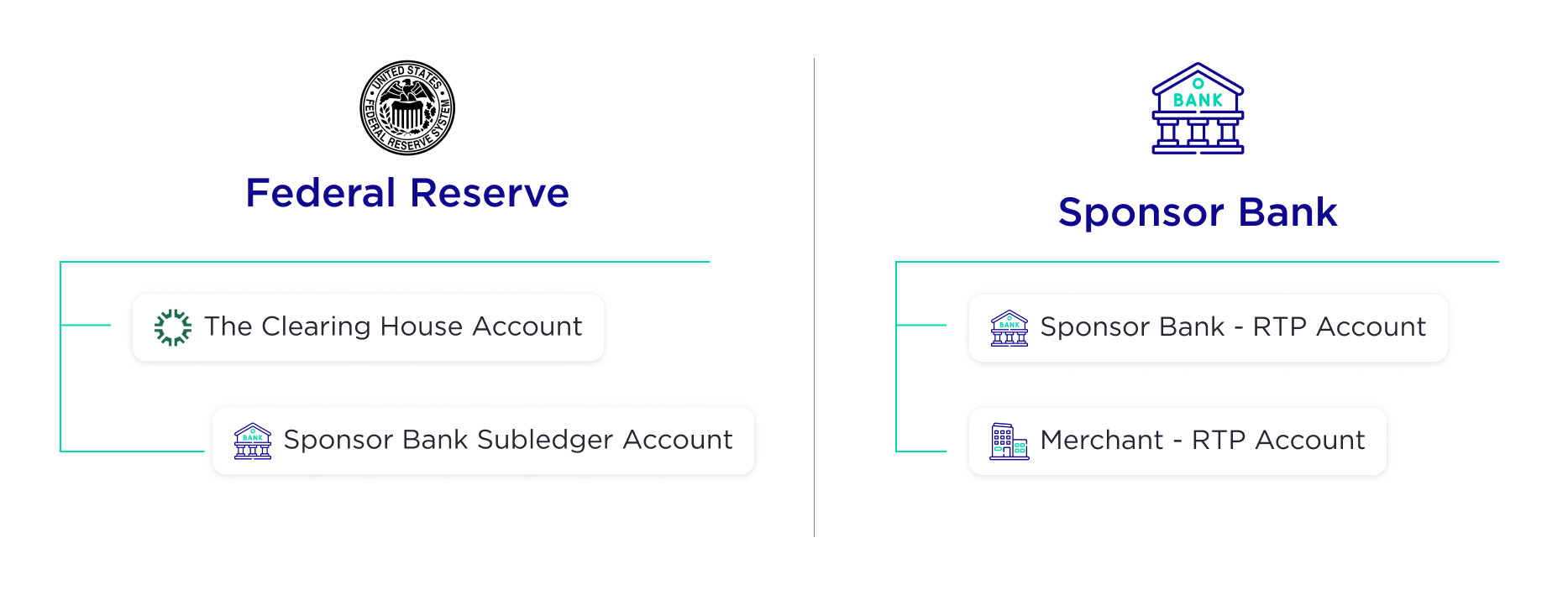

| TCH-Sponsor Bank account | TCH has an account at the Federal Reserve Bank. Sponsor Bank has a subledger account within the TCH Federal Reserve Bank account. |

| Sponsor Bank-RTP account | Sponsor Bank will establish an RTP funding account at Sponsor Bank to hold monies due for RTP credit instructions. It is responsible to maintain sufficient funds for inbound credit transfers to the merchant, and for mirroring aggregate merchant balances for outbound credit transfers. |

| Merchant RTP Account | Each merchant has a dedicated account at Sponsor Bank for RTP Credit Transfers. This account can be a Beneficiary Account for receive-only accounts (Merchant Beneficiary Account). This account can be a Prefunded Account for send-only or sending and receiving accounts. |

| Merchant Beneficiary Account* | Each merchant has a dedicated account at Sponsor Bank to receive incoming credits. *Receiving only does not require pre-funding. |

| Merchant Prefunded Account | Each merchant has a dedicated account at Sponsor Bank that holds their prefunded balance for outbound transfers. |

Sponsor Bank - Account Management

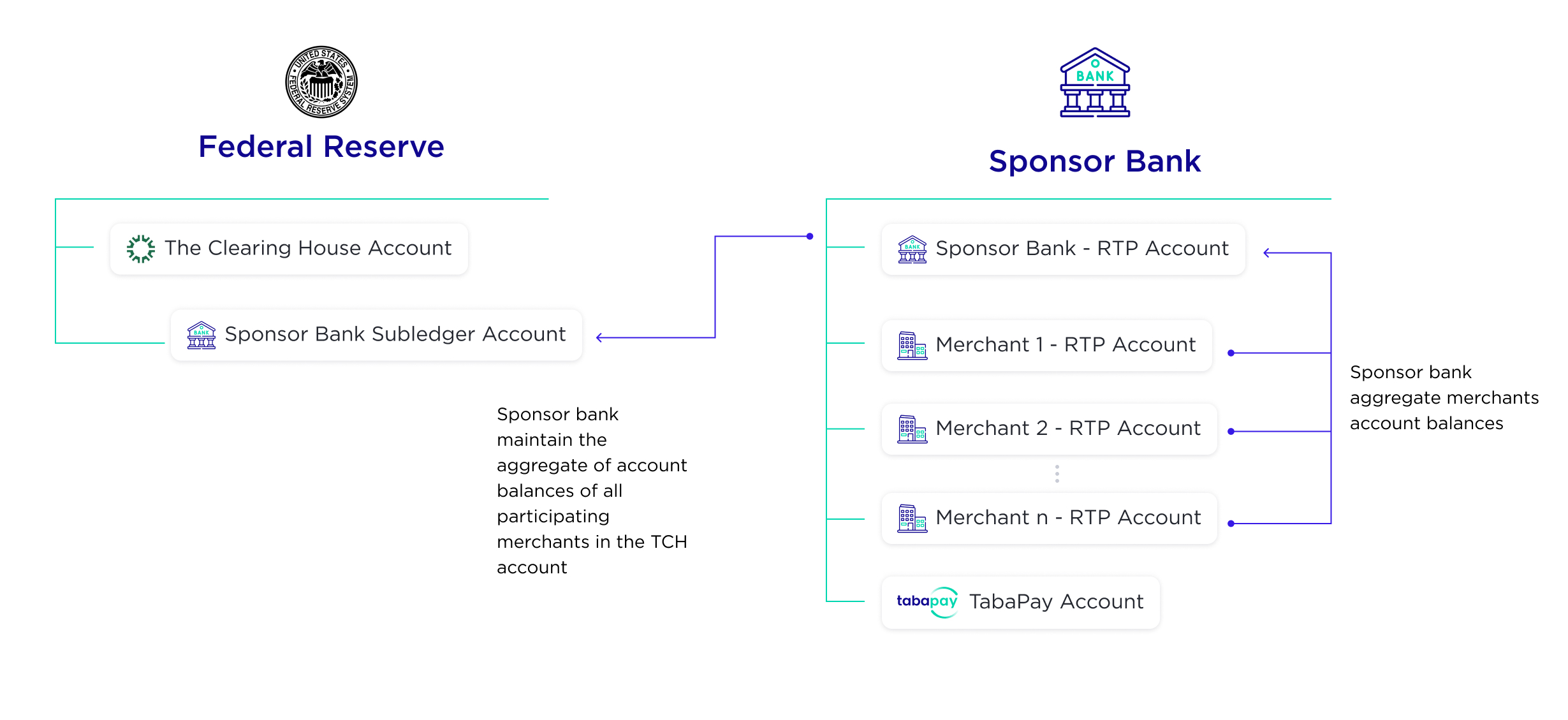

- Sponsor Bank is responsible for providing sufficient funds in the TCH-Sponsor Bank Fed account to keep daily payments flowing. Sponsor Banks send funds to their TCH-Sponsor Bank account via Fedwire to fund.

- Each merchant has a dedicated RTP account at Sponsor Bank. Sponsor Bank is responsible for maintaining a balance in the TCH-Sponsor Bank account equal to the aggregate of account balances of all participating merchants.

- To keep up with the balances, Sponsor Banks send funds to their TCH-Sponsor Bank account via Fedwire to fund as required.

The management of accounts at the Sponsor Bank for dedicated merchant accounts and subsequent balance maintenance at the TCH-Sponsor Bank account is out of scope of TabaPay.

Real-time Balance Check

- Sponsor Banks must maintain running total of each merchant’s RTP account to ensure that there are enough funds in the Merchant Prefunded Account.

- For every outbound credit transfer request from the merchant, TabaPay will post the request with the Sponsor Bank to check if there are sufficient funds in the Merchant Prefunded Account at the Sponsor Bank before allowing the credit transfer request to go through The Clearing House.

Controls and Limits

The following controls and limits govern the flow of funds to and from TCH RTP.

Governing outbound credit transfers

All the following governors are independent i.e., when any one governor is triggered, it will stop outbound credit transfers.

- Sponsor Bank must authorize each outbound credit transfer, and Sponsor Bank only authorizes if sufficient funds are available in the Merchant Prefund Account. (Step 3 in Figure 3: Outbound Credit Transfer)

- Sponsor Bank moves each authorized outbound credit transfer from the Merchant Prefund Account (Step 3 in Figure 3: Outbound Credit Transfer). The merchant must have sufficient funds in its dedicated Merchant Prefunded Account with Sponsor Bank (Merchant RTP Account at Sponsor Bank)TabaPay maintains a maximum daily limit a merchant may originate.

- Total Sponsor Bank daily limit is governed by the total funds in the TCH-Sponsor Bank Fed account. This account must be maintained for smooth payments flow and cannot go negative.

- Sponsor Bank can lock (or unlock) a merchant on the TabaPay system.

The governance of outbound credit transfers has multiple controls to prevent a merchant from overdrawing their Merchant Prefunded Account.

-

Sponsor Bank Authorization: Each outbound credit transfer must be authorized by Sponsor Bank prior to TabaPay posting the PACS.008 credit transfer message to TCH. TabaPay invokes authorization request with Sponsor Bank prior to posting the credit transfer to TCH. If a negative or ‘no response’ is received from the Sponsor Bank, then TabaPay does not originate the credit, and the merchant receives a negative response from TabaPay.

-

Merchant Prefunded Account Balance: Each Merchant Prefunded Account is a dedicated RTP account at the Sponsor Bank. When Sponsor Banks authorize the outbound credit transfer, money is moved from the Merchant Prefunded Account to the Sponsor Bank – RTP Account. Sponsor Banks, however, will not authorize a payment if the Merchant Prefunded Account has insufficient balance prior to debiting the account. Without Sponsor Bank’s successful authorization, the credit transfer is not originated by TabaPay.

-

TabaPay limits: TabaPay maintains a maximum daily disbursement amount (ceiling) for each merchant. This daily amount resets daily at settlement.

-

Sponsor Bank Maximum Limit: TCH requires good funds in the TCH-Sponsor Bank Fed Account. Sponsor Bank operations will fund this account with the aggregate monies in all the Sponsor Bank’s individual Merchant Prefunded Accounts. At each reconciliation window during the day, the following is checked and reconciled:

a. Aggregate funds in the Merchant Prefunded Accounts

b. Balance in the TCH-Sponsor Account -

Sponsor Bank Merchant Controls: Sponsor Bank can lock or unlock a merchant at any time, which suspends or enables a merchant’s ability to originate RTP credits.

An active merchant can be locked by clicking “Lock” – see sample below

A locked merchant can be unlocked by clicking “Unlock” – see sample below

Merchant authorization for outbound transfers

Merchant approval for each credit origination is received as follows:

- A sponsor bank can opt for merchants to digitally sign the transaction request with secure credentials provided by Sponsor Bank (when the merchant opened their account at the Sponsor Bank.) This secure digital signature would provide non-repudiation for Sponsor Bank to debit the merchant account.

- Merchants must use their API credentials provided by TabaPay. The credentials are provided through a secure link when merchant register for the RTP program with TabaPay.

- Merchants must initiate the API request from an IP address registered with TabaPay. During merchant registration, merchants are responsible for providing their IP addresses to be whitelisted at TabaPay.

Governing inbound credit transfers

When TabaPay receives inbound credit transfers, credits are made to the Merchant Beneficiary Account at the Sponsor Bank.

TabaPay routes these transfers to Sponsor Banks. TabaPay digitally signs the transfer with secure credentials provided by Sponsor Bank during the TabaPay-Sponsor Bank integration. Any transaction initiated from TabaPay to Sponsor Bank without this digital signature is denied.

Any credit transfer received by TabaPay from TCH for the merchant will be routed to Sponsor Bank.

How RTP Works

Create Transaction API allows you to send, receive, and request to pay. Specify type R for RTP in achOptions, along with Account Number and Routing Number (Push or Pull depending on whether it is Send or Receive).

API Request for RTP

To generate an RTP transaction, include achOptions: R to designated the RTP TCH network.

Note: This is an abbreviated request, for the full request, refer to RTP Push Transaction, or Create Transaction API.

{

"referenceID": "myUniqueRefID3",

"...",

"achOptions": "R",

"amount": "100.00"

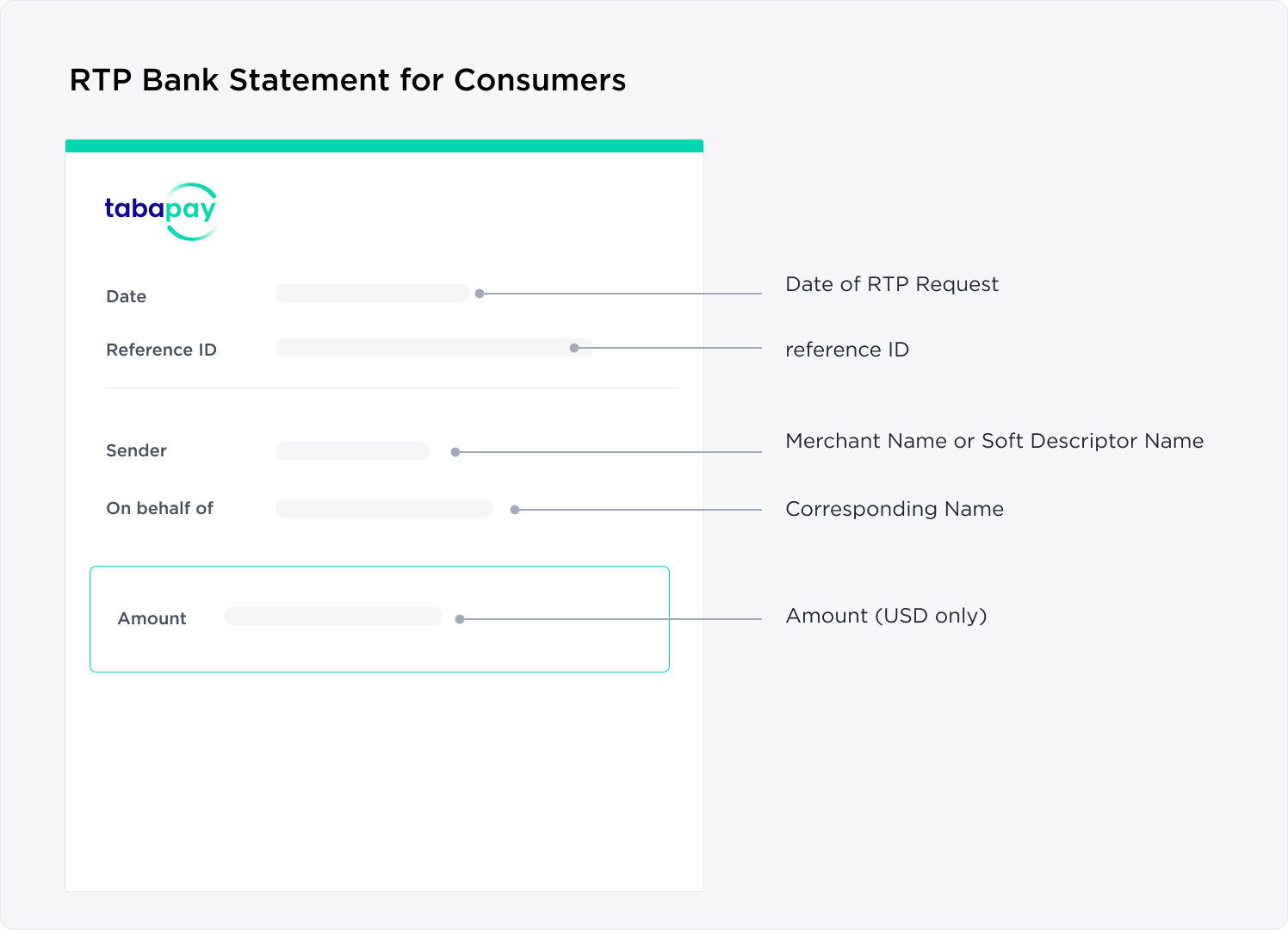

}RTP Bank Statement for Consumers

Code Samples

Learn how RTP works using the TabaPay API.

Updated 4 months ago